All Categories

Featured

Table of Contents

The strategy has its very own advantages, however it additionally has problems with high charges, complexity, and more, leading to it being considered a scam by some. Boundless financial is not the most effective plan if you need only the investment part. The limitless financial principle focuses on making use of whole life insurance policy policies as a financial tool.

A PUAR permits you to "overfund" your insurance coverage right up to line of it becoming a Modified Endowment Contract (MEC). When you utilize a PUAR, you quickly boost your cash worth (and your survivor benefit), therefore increasing the power of your "bank". Further, the more money value you have, the better your rate of interest and returns payments from your insurance provider will be.

With the surge of TikTok as an information-sharing platform, monetary suggestions and methods have discovered an unique way of spreading. One such approach that has actually been making the rounds is the limitless banking principle, or IBC for brief, garnering recommendations from celebrities like rap artist Waka Flocka Flame - Infinite Banking retirement strategy. While the method is presently preferred, its roots trace back to the 1980s when financial expert Nelson Nash presented it to the globe.

How does Infinite Banking For Retirement compare to traditional investment strategies?

Within these plans, the cash value grows based upon a price set by the insurance company. Once a substantial money value accumulates, insurance holders can acquire a cash money value finance. These lendings vary from traditional ones, with life insurance coverage offering as security, indicating one can shed their insurance coverage if borrowing excessively without ample money value to sustain the insurance policy expenses.

And while the attraction of these policies appears, there are natural limitations and threats, necessitating thorough cash worth tracking. The approach's legitimacy isn't black and white. For high-net-worth individuals or company owners, specifically those utilizing approaches like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and substance development can be appealing.

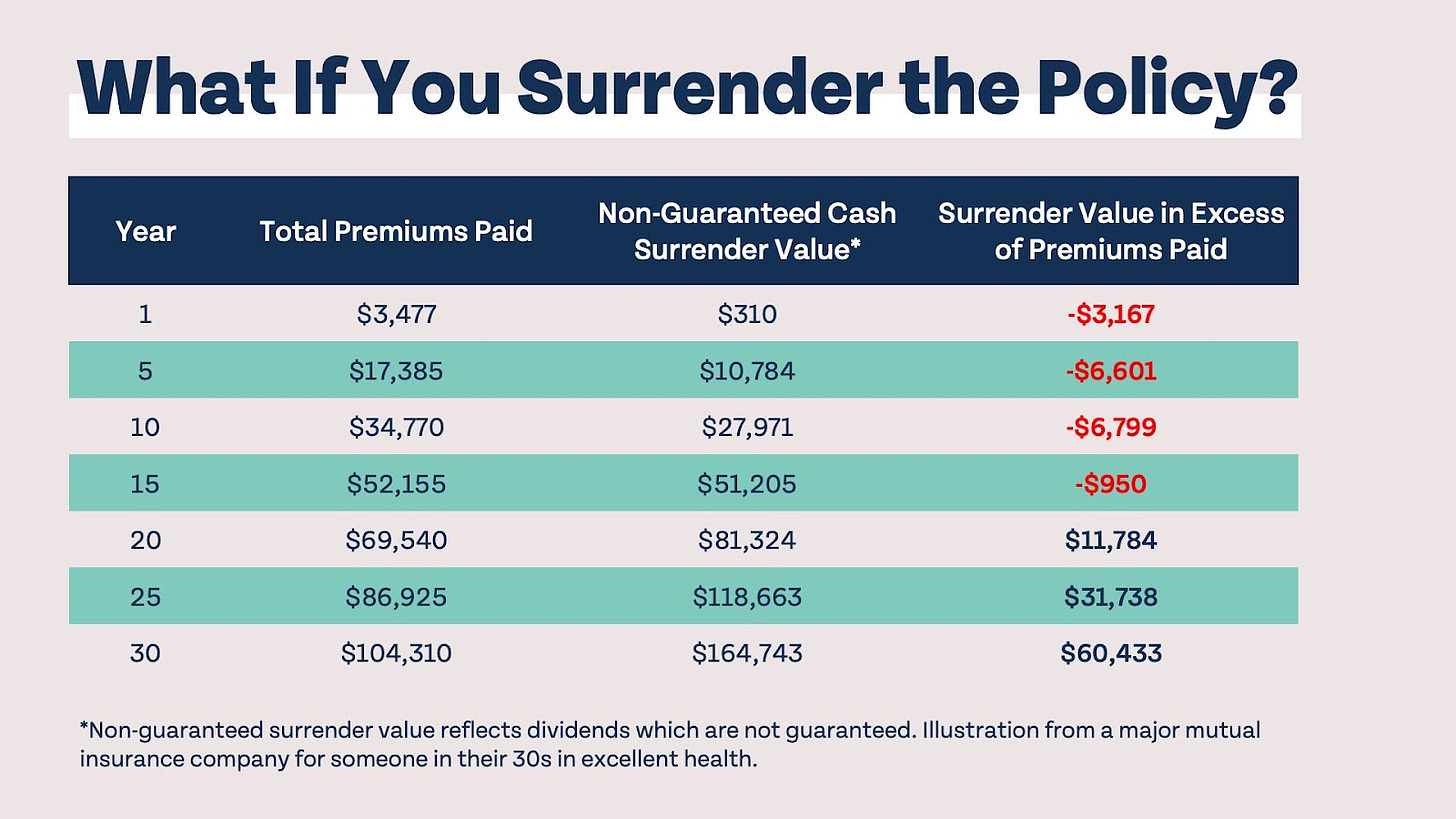

The attraction of limitless banking does not negate its obstacles: Expense: The fundamental need, an irreversible life insurance policy policy, is more expensive than its term equivalents. Eligibility: Not everybody gets approved for entire life insurance policy due to extensive underwriting procedures that can omit those with specific health and wellness or lifestyle problems. Intricacy and threat: The intricate nature of IBC, paired with its threats, may prevent numerous, particularly when less complex and much less high-risk choices are available.

How do I optimize my cash flow with Wealth Management With Infinite Banking?

Alloting around 10% of your monthly earnings to the policy is just not practical for many individuals. Using life insurance policy as an investment and liquidity source needs technique and tracking of policy cash value. Seek advice from a financial advisor to identify if infinite banking lines up with your concerns. Part of what you read below is merely a reiteration of what has actually currently been claimed over.

So prior to you obtain into a scenario you're not prepared for, recognize the adhering to first: Although the principle is commonly offered thus, you're not in fact taking a financing from on your own. If that were the case, you wouldn't need to repay it. Rather, you're borrowing from the insurance coverage company and need to settle it with rate of interest.

Some social networks posts recommend making use of cash money worth from entire life insurance policy to pay for charge card debt. The idea is that when you repay the lending with passion, the quantity will certainly be returned to your financial investments. That's not just how it works. When you pay back the financing, a portion of that rate of interest goes to the insurance provider.

What are the most successful uses of Policy Loan Strategy?

For the very first a number of years, you'll be settling the compensation. This makes it extremely tough for your plan to build up worth during this time. Entire life insurance policy expenses 5 to 15 times more than term insurance. A lot of individuals simply can not afford it. Unless you can pay for to pay a couple of to several hundred dollars for the next years or more, IBC will not work for you.

If you need life insurance coverage, right here are some important ideas to think about: Think about term life insurance. Make certain to go shopping about for the ideal rate.

How flexible is Wealth Building With Infinite Banking compared to traditional banking?

Imagine never having to worry regarding financial institution financings or high rate of interest prices again. That's the power of infinite banking life insurance policy.

There's no set loan term, and you have the freedom to pick the settlement timetable, which can be as leisurely as paying back the financing at the time of death. This flexibility encompasses the maintenance of the lendings, where you can go with interest-only settlements, maintaining the loan balance flat and workable.

How does Infinite Banking In Life Insurance compare to traditional investment strategies?

Holding money in an IUL dealt with account being attributed rate of interest can commonly be much better than holding the cash money on down payment at a bank.: You have actually always imagined opening your own bakery. You can obtain from your IUL policy to cover the first expenditures of leasing an area, acquiring tools, and hiring staff.

Personal loans can be obtained from typical banks and credit unions. Below are some vital points to think about. Charge card can give an adaptable means to borrow cash for very temporary durations. Nonetheless, borrowing cash on a charge card is generally very expensive with interest rate of rate of interest (APR) often getting to 20% to 30% or even more a year.

{kind=link}

Latest Posts

How To Be Your Own Bank In Just 4 Steps

Profile For Be Your Own Bank

Is "Becoming Your Own Banker" A Scam? (2025)